Arizona R&D Credit

With Tax Robot, Arizona’s R&D Tax Credit becomes more than a benefit—it becomes a catalyst for your business growth. Unleashing the incredible, simplifying the complex. This is not just tax planning; it’s financial evolution.

Maximize your State Credits today!

Put the R&D tax credit process on autopilot.

Trusted By:

Arizona R&D Tax Credits

Discover your eligibility for Arizona R&D tax credits and supercharge your enterprise.

Arizona’s Research and Development Incentive

The Arizona R&D credit applies to any corporation or individual working in Arizona. You can claim 24% of the first $2.5 million spent on qualifying research and development activities. You can also claim 15% of your money on activities over $2.5 million. There is no cap on how much money you can claim or how big your expenses are.

You can claim an additional credit if you pay for research from an Arizona college or university. You can receive 10% of the money you spend in excess of $2.5 million, plus the standard credit of 15%. Your company can carry any unused credits forward for the next 15 years, though they will expire if you don’t claim them.

Title 16, Section 41 of the Internal Revenue Code defines the qualifying research activities for Arizona taxpayers. You can claim the money you spent on paying your research employees and buying research supplies, including items for manufacturing your products. You can also claim 65% of the money you spend on hiring outside experts for research, such as university professors and lawyers.

The tax credit will last until 2030. After 2031, you can claim only 20% of the first $2.5 million you spend and 10% of your additional expenses.

Example of Arizona’s Incentive

Let’s say an Arizona company spends $3 million on research and development in 2023. 24% of the first $2.5 million of expenses equals a dollar-for-dollar tax credit of $600,000. The company can then claim 15% of the remaining $500,000 in expenses, which equals $75,000. This means that the Arizona corporation can claim $675,000 in credits.

How its calculated

You must fill out Arizona Form 208 to receive your credit. You must provide exact figures on how much your supplies and research professionals cost. Arizona’s government does not require you to attach corroborating documents to your form, but you should have them on hand to prove your claim in case the government audits you. Practice good startup bookkeeping strategies so your information is easy to find and collect.

You can use the same form to claim refundable and non-refundable credits. If you are in a partnership, you must mention that on your form. You and your partner will share the R&D credits based on how much you contributed to your research expenses.

Do not submit your forms until an R&D professional has looked at them. Calculate your claims multiple times to fix any mistakes and get the full amount you deserve.

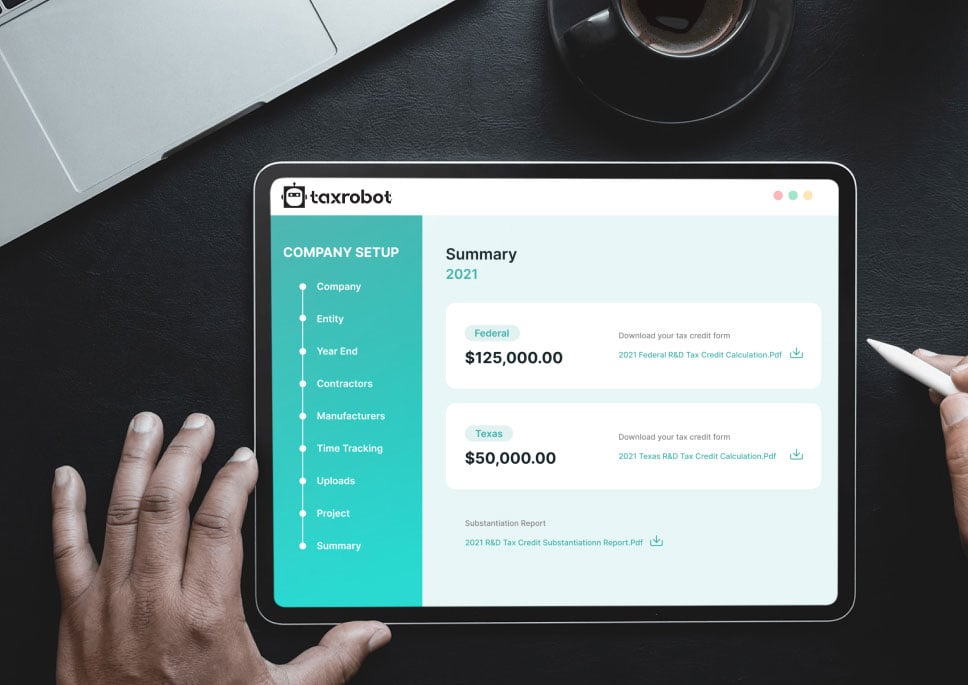

Take a sneak peak

- Limited Time Offer

- Simple Onboarding

- Easy to Use

R&D Tax Credits FAQs

The four-part test as outlined in the Internal Revenue Code is used to determine qualified R&D activity.

The Four-Part Test

1). New Or Improved Business Component

Creation of a new product, process, formula, invention, software, or technique; or improving the performance, functionality, quality, or reliability of existing business component.

- Construction of new buildings or renovation of existing buildings

- Invention of a software application

- Manufacturing of a new product or the improvement of the production process for an existing product

- Creation of design documentation

2). Technological In Nature

The activity fundamentally relies on principles of the physical or biological sciences, engineering, or computer science. A taxpayer does not need to obtain information that exceeds, expands or refines the common knowledge of skilled professionals in a particular field.

- Physics (relationship between mass, density and volume; loading as the

result of gravitational attraction) - Engineering (mechanical, electrical, civil, chemical)

- Computer science (theory of computation and design of computational systems)

3). Elimination Of Uncertainty

Uncertainty exists if the information available to the taxpayer does not establish the capability or method for developing or improving the business component, or the appropriate design of the business component.

- The capability of a manufacturer to create a part within the specified tolerances

- The appropriate method of overcoming unsuitable soil conditions during construction

- The appropriate software design to meet quality and volatility requirements

4). Process Of Experimentation

A process designed to evaluate one or more alternatives to achieve a result where the capability or method of achieving that result, or the appropriate design of that result, is uncertain as of the beginning of the taxpayer’s research activities.

- Systematic process of trial and error

- Evaluating alternative means and methods

- Computer modeling or simulation Prototyping Testing

The R&D tax credit is one of the most misunderstood tax incentives available. Considering the myriad of industries and activities that legally qualify for the credit, the term “research and development” is a misnomer. Additionally, the R&D tax credit requires specialized knowledge and technology to identify and calculate the incentive properly.

Companies of various industries are unaware that they are eligible to claim the R&D tax credit. Under the Internal Revenue Code’s definition of R&D, many common activities qualify. You can get tax benefits for industries including software, technology, architecture, engineering, construction, manufacturing, and more.

The R&D tax credit can be claimed for all open tax years. Generally, open tax years include the prior three tax years due to the statute of limitations period. In certain circumstances, the law allows businesses to claim the R&D tax credit for an extended period of time. It is common for companies to amend previous tax years to claim this benefit and reduce the maximum amount of tax liability.

Partnerships and S corporations must file this form to claim the credit. The credit will flow from the Form 6765, to the Schedule K-1, to the Form 3800 on the individual’s tax return. For individuals receiving this credit that have ownership interest in a partnership or S corporation, Form 6765 is not required on the individual return.

Individuals claiming this credit can report the credit directly on Form 3800, General Business Credit if their only source for the credit is a partnership, S corporation, estate, or trust. Otherwise, Form 6765 must be filed with the individual’s tax return (e.g. sole proprietorship).

For tax years prior to 2016, the credit can be used to reduce the taxpayer’s regular tax liability down to the tentative minimum tax. The credit cannot be used to offset alternative minimum tax. Beginning in tax year 2016, eligible small businesses have expanded utilization for the credit. For these eligible small businesses, the regular tax liability can offset alternative minimum tax using the “25/25” rule.

What our customers have to say

I highly recommend TaxRobot to anyone considering an R&D Tax Credit software to complete their analysis.

We decided to switch to TaxRobot… Best decision we’ve ever made. More affordable, and less complicated.

I couldn’t believe how easy it was! In under an hour, we saved enough money to hire a new employee.